Hidden gold nuggets in mining news releases

By Paul Harris, Editor Gold Journal

Potentially rich insights in the fine print of two leading Canadian gold juniors, Snowline Gold and Newfound Gold

Gold: US$1,720/oz, YTD -5.7%, 30 day -3.9%

At GoldJournal, we look for anomalous information in mining news releases– something surprising or significant which may inform a story or a trade.

Often these cues are subtle. Such as what a company does not say.

Here are two recent examples.

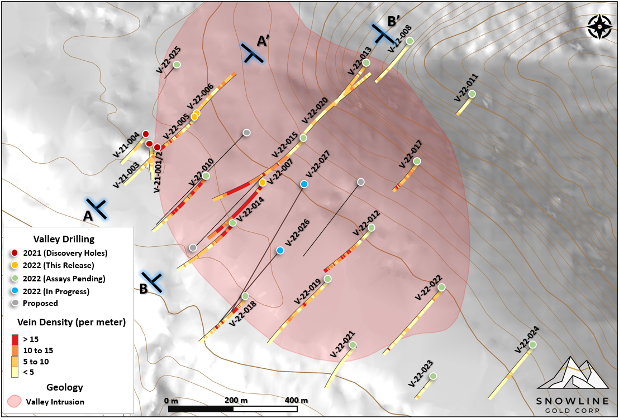

Yukon, Canada gold explorer Snowline Gold (SGD:CSE, C$289M) has been a hot stock this summer for good reason. Their virgin gold discovery at the Rogue prospect has yielded significant intercepts, such as 282.9m @ 2.3g/t Au announced August 24.

The news release announcing the find was the first GoldJournal has ever seen to include vein density AND gold grade. The cross section clearly shows a correlation between vein density and higher-grades:

I spoke with CEO Scott Berdahl about this, who told me the inclusion of this information stems from the work of company chair Craig Hart on reduced intrusion-related gold systems in the early/mid 2000s. For those of you who want to get more technical, read his paper here, particularly on p97.

Where this observation gets interesting is when you look at the traces of the drill holes drilled but not yet reported. To date the company has reported holes 1 through 7 with hole 7 producing the big intercept mentioned above. Looking at the plan view, Snowline has drilled up to hole 24. Holes 10, 12, 14 and 15 were drilled within a couple of hundred metres of hole 7 and have intercepts which contain good vein density, so we could assume these holes will return some good grade gold intercepts.

“With the lab backlog, the vein densities and amount of quartz – as well as presence of VG (though that’s really more of a non-exclusive binary indicator) – are really all we have to go on. It’s not perfect, but it tells us a lot about whether we’re hitting or not as well as what we’re hitting, which is a blessing for a gold-only target,” said Berdahl.

Scott added that, “ultimately, knowing what we know of these systems, and seeing what we saw in the core, we decided these visuals were material information, as they demonstrated the presence of a large, intense system, though of course we still didn’t know grade with any certainty,” he said.

When we look at some of the big step-out holes to the east though, such as 8, 11, 21, 22, 23, 24, they do not seem to be carrying high vein density. Should we therefore assume they will not carry good gold grade and that Valley could be closed off to the east? As Rogue is an intrusion-related deposit, we would expect to see a strong core zone where the intrusion is, and lower vein density (and grade?) in the step-outs suggests the company is finding the edges of the intrusion.

The caveat is that any single vein could carry a lot of gold and you never know for certain until you get the assay results from the lab. This caveat could be important as Snowline also reported that there was visible gold in holes 21 and 22.

“As you suggest, low vein densities do not necessitate low grades, and vice versa. Not perfect, but it tells us a lot,” said Berdahl. Scott referred to the photo of hole 5 attached to the above release as an example of the latter. This interval returned an average of 1.09g/t Au. “That was one of the flashier sections from that hole, but it was below average for the interval it was in,” he said.

Rogue is looking like it will have a significant, near surface, core with high vein density of 1-2 g/t, with the kicker being a much larger ring of moderate vein density around it at just under 1 g/t.

Berdahl expects the C$950/m drilling costs figure to come down as production efficiencies come further into play. “Should we double down into detailed resource drilling, we should bring those costs down substantially through ground supported drilling,” he said.

Queensway

Across the other side of Canada, Newfound Gold (TSX:NFG, C$757M) has been a darling stock due to a string of very high-grade intercepts at its Queensway project in Newfoundland-Labrador. It has seen a massive influx of investment including from legendary investor Eric Sprott (his largest personal investment) which propelled its market capitalization to around C$2B at its peak!

The company is in the midst of a whopper 400,000m drilling program, and once again, the interesting story may be in what the company isn’t saying rather than the double-digit grams per tonne it reports on a regular basis.

In Newfound’s May technical report the company says it has drilled 697 holes for 192,000m. In its September 1 news release it said it has completed about 250,000m of the 400,000m program, and it reported up to hole 675 with a highlight of 5.75m @ 18.95g/t. More metres, but check out the hole number. It also said it has 38,000m of core at the assay lab.

Time for some bad math.

On page 15 of its September 2 corporate presentation it says: “The deepest drill hole to date has gone to less than 400m, while a majority of drilling has focused on the first 200m from surface,” and it includes a section with the drill plots.

Let’s assume an average depth of 250m, which would mean Newfound Gold has drilled 1,000 holes so far to get to its 250,000m total.

At an average of 250m per hole, the holes at the lab represent another 152 holes, which would bring its total holes to 827.

So the question is whether there are 173 holes (1,000 assumed holes less the 827 presumed holes drilled based on the publicly released data) for 43,250m drilled and unreported? And if so why? Were these all dusters, holes carrying little or no grade?

NewFound Gold did not respond to my requests for clarification on this issue, although that could be more to do with Labor Day than avoiding the question per se.

Big drill hits powered NewFound Gold to a C$2B market capitalisation. Its Queensway project is an orogenic gold system which can be difficult to explore, prove continuity and ultimately mine.

To paraphrase a well-known saying, a few good drill hits do not make a project. Newfound has returned more than a few good drill hits, but if the gap in its drill hole reporting does exist it could mean Queensway may not be the slam dunk many people think it is.

Not the first time

Absent holes is an issue that crops up from time to time. I spoke with Joe Mazumdar of Exploration Insights about this issue and he refered me to a graphic he put in one of his newsletter. Mazumdar said this visual illustrates how incomplete drill hole reporting and can lead to unrealistic mineralisation volume estimates.

Mazumdar saw this situation with Dalradian Resources at its gold project in Northern Ireland, which ultimately resulted in him selling the stock. For the record, EI sold at C$1.22 per share, below the C$1.47 takeout price offered in 2018 by Orion Mine Finance, which faces community resistance to build the mine.

“We expressed our concern regarding a number of unreported drillhole results from the recently completed +50,000m infill drilling program. After a detailed review of all the publicly available data, we concluded that the data gaps, and more importantly, the lack of grade continuity along the veins, are significant enough to negatively impact the pending resource estimate update and, consequently, the mine economics,” he wrote at the time.

Similar disclosure issues were also part of past market disappointment at Canaco Resources’ Magambazi gold deposit in Tanzania almost a decade ago. Here, the company finally released missing drill holes in a 117-hole data drop one week prior to publishing a much delayed resource estimate.

The May 2012 indicated resource contained 721,300oz with another 292,400oz inferred which disappointed the market as a Bay St anaylst had been forecasting more than 3Moz! Canaco’s share price chart traced a ballistic rise and fall, and the company became Orca Gold in 2013.

A more well-known example is Rubicon Minerals and its Phoenix deposit in the Red Lake district of Ontario, Canada which resulted in the collapse of that company, a restructure, a multi-year rescue by George Ogilvy and his team, and eventual sale to Evolution Mining in 2021.

Another recent example is Novo Resources (TSXV:NVO, C$107M) and its Purdy’s Reward gold project in Western Australia, where Mazumdr saw a “difficulty in accurately sampling this deposit” due to the “considerable variability in the grade, thickness and number of gold bearing horizons”.

You get the point.

Anza

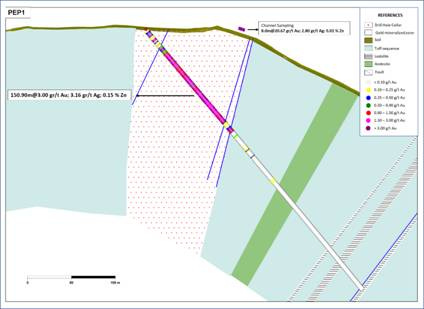

One final one news release to mention here, Orosur Mining’s (AIM:OMI; C$47M) Anza gold project in Antioquia, Colombia. The company reported a hit of 150.9m @ 3g/t Au from surface at the Pepas target this week, which saw its share price jump a tidy 43% in London.

Here, the company deliberately withheld locational information at the request of its JV partners so as not to give clues to illegal miners of where it is getting good hits. In a mining context, one of the meanings of Pepas is gold grains or nuggets.

“Agnico [Eagle Mines] and Newmont changed the prospect names and asked us not to show any maps to not attract illegal miners. Where maps are used they are without coordinates,” said CEO Brad George during a webinar.

Exploration is all about opportunity and risk management after all and Newmont’s former investment in Continental Gold, whose Buritica deposit is about 50km from Anza, was plagued by invasions of illegal miners. To this day illegal miners are a serious headache for Zijin Mining, which bought Continental in a C$1.4B all cash deal in 2020.

I’m of the opinion The West as a whole needs a brand new system — made in the 21st century for the 21st century using the following themes:

- simplicity

- standardization (silly humanity tries to accomplish the same goals a million different ways — pick the best and use it until a better option comes down the pipe)

- economies of scale

- free and open data for circular accountability

- basic income (AI and technology is going to create massive gains in economic output so can easily afford this)

I believe a federal - municipal system would be best. Mayors can be elected by their local constituents; then the mayors can elect a leader/dictator who has a great deal of power to push forward their agenda, with a veto mechanism to prevent them going off the rails (mayors have the vote for the veto, but make it high like 75% for example so you need a strong consensus to veto the leader).

Create a constitution made in the 21st century for the 21st century.

Create a system so good that everyone wants in as the benefits will be so immense that only fools will stay out (a better quality of life and economic outcomes). Could likely start this system in Canada and go after the low hanging fruit that is The Commonwealth.

The arc of humanity and civilization is unification — I believe we are seeing the late stages of nationalism (which is fragmentation and wars). I believe we must live through this chaotic WW3 era before my grand plan door opens.

The Newfound Gold analysis above makes a huge rookie mistake by confusing depth from surface with the length of the drill holes. Their math would be correct if the holes were vertical, but they are drilled at a much more shallow angle. This fact nullifies their entire thesis.